VC funding drops 47%, deal activity climbs - a look at 🇨🇦 climate venture in H1/23

Deal activity is up in climate, but total funding and deal sizes are down, mirroring similar shifts in global climate venture. Plus a look at venture activity and who's leading rounds

Hey there,

Happy Saturday! Today we’re taking a look back at the first half of 2023 and the state of climate venture funding in Canada. Main trends at a glance:

Less capital deployed into climate tech overall

More deals being closed year-over-year, but at smaller sizes

Continued focused on Energy, Industry, and Food/Land Use

You can check out our deep dive into Q1 here. Some of the figures have changed as I’ve honed how I’m tracking these rounds. I’ve included a note about methodology at the end if you’re interested.

Let’s get into it!

H1/23 at a glance

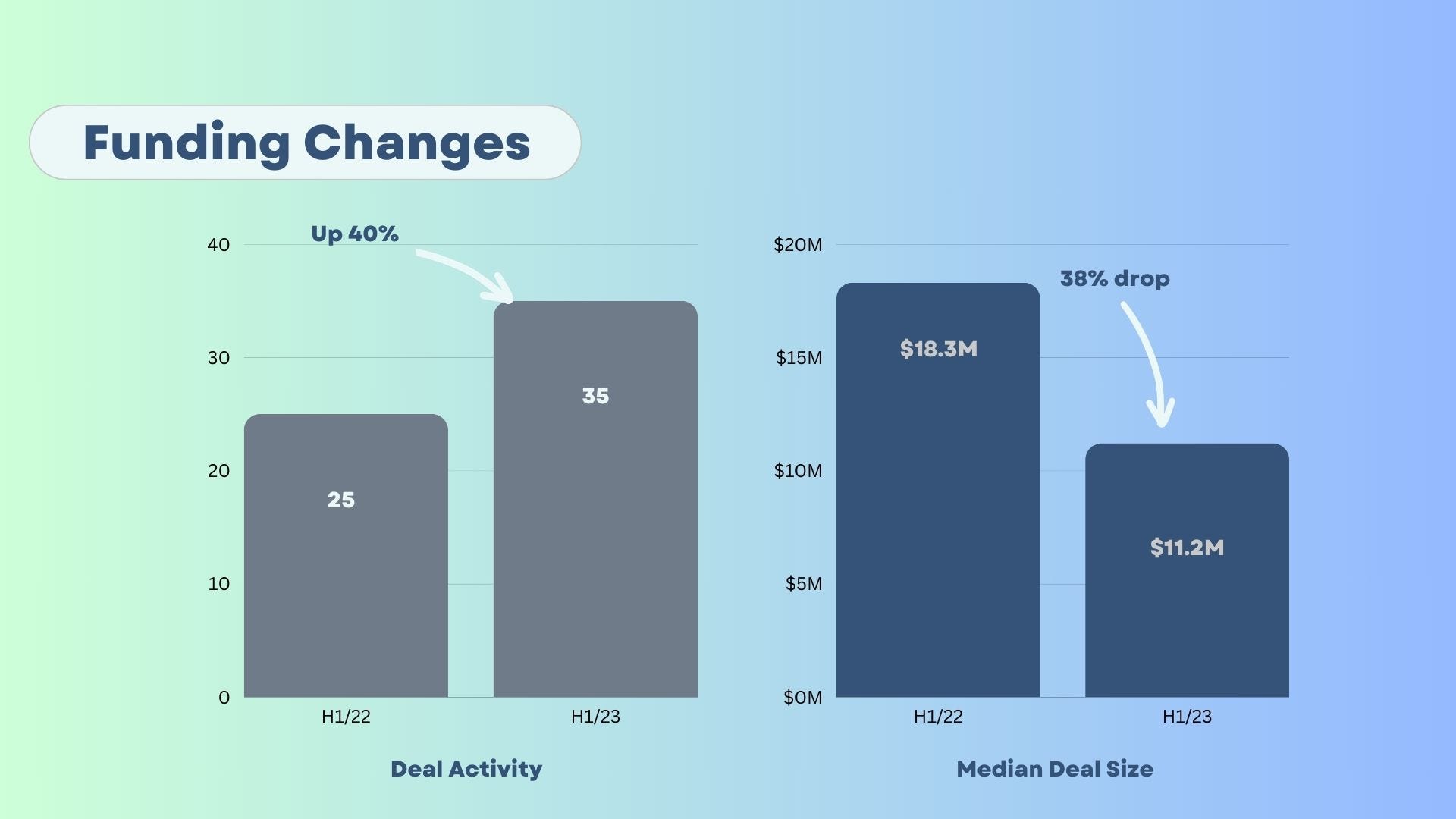

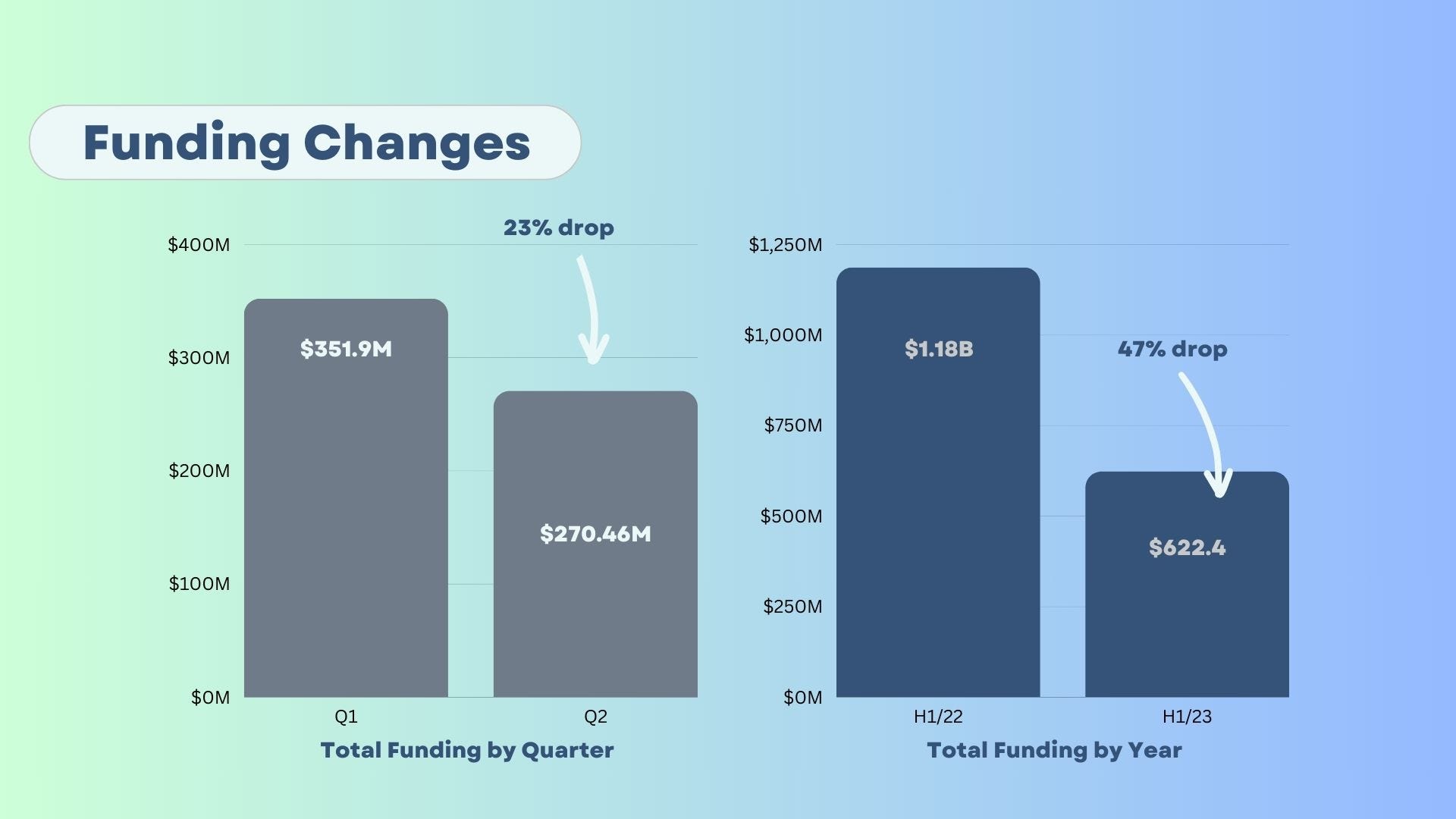

In the first six months of the year, we saw 35 rounds totalling more than $622M raised. Notable rounds this quarter include Eavor’s $80M Series B, Peak Power’s $47M growth round and $27M Series As from both BrainBox AI and Cyclic Materials.

One trend stood out when looking both by quarter and year-over-year: deal volume has increased, while median deal size has gone down:

It’s almost a 1-to-1 change, with a 40% increase in volume and 38% decrease in median deal size.

The result: a ~47% drop in total capital deployed in H1/23 compared to H1/22.

Where’s funding going?

By Stage

H1/23 continued to see a strong focus on early stages as Pre-Seed to Series A made up 56% of deals. We also had more activity in Series B+ rounds, with 7 in H1/23 vs just 2 in H1/22.

The average size of Seed rounds increased by 36.5%, going from $5.2M in 2022 to $7.1M in 2023. This was driven a few small seed rounds like New School Foods’ $15.9M raise and Future Fields’ $15.1M Seed extension.

By contrast, the average size of Series A rounds dropped 30% from $32.9M in 2022 to $23M in 2023.

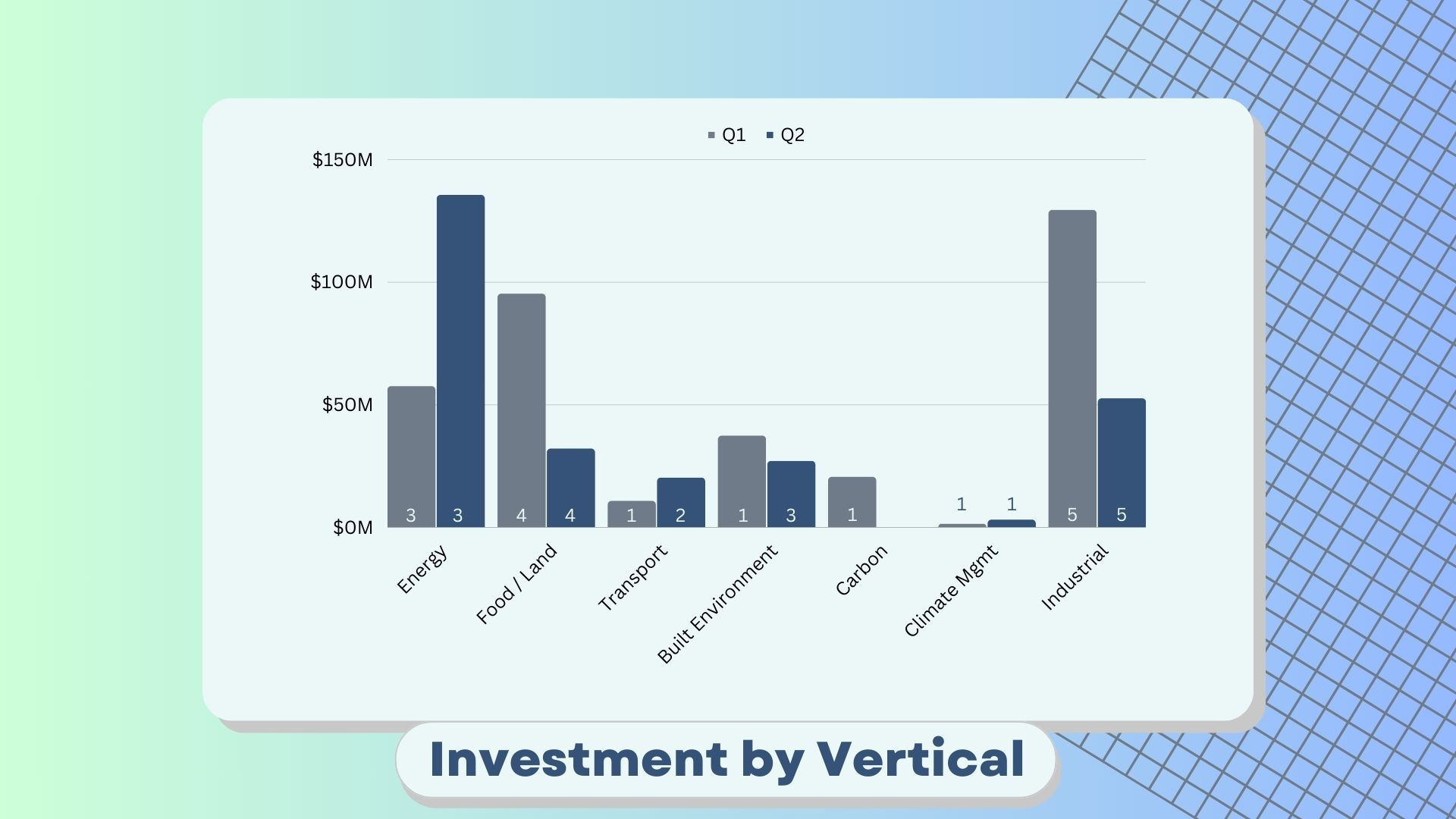

Climate vertical

Industry, Food & Land Use, and Energy continue to be the most active verticals quarter-over-quarter. The most capital was deployed to Energy and Industry with $135.5M and $52.6M respectively.

Here you can see the shift to smaller deal sizes: Industry had 5 rounds in both quarters, but secured $76.8M more in Q1 vs Q2. Food & Land Use saw a similar change, from $95.2M in Q1 to $32M in Q2.

Notable gaps: Carbon, Climate Management and Transport. These verticals featured just 2-3 rounds each, and together raised less than the next largest category, Built Environment.

Region

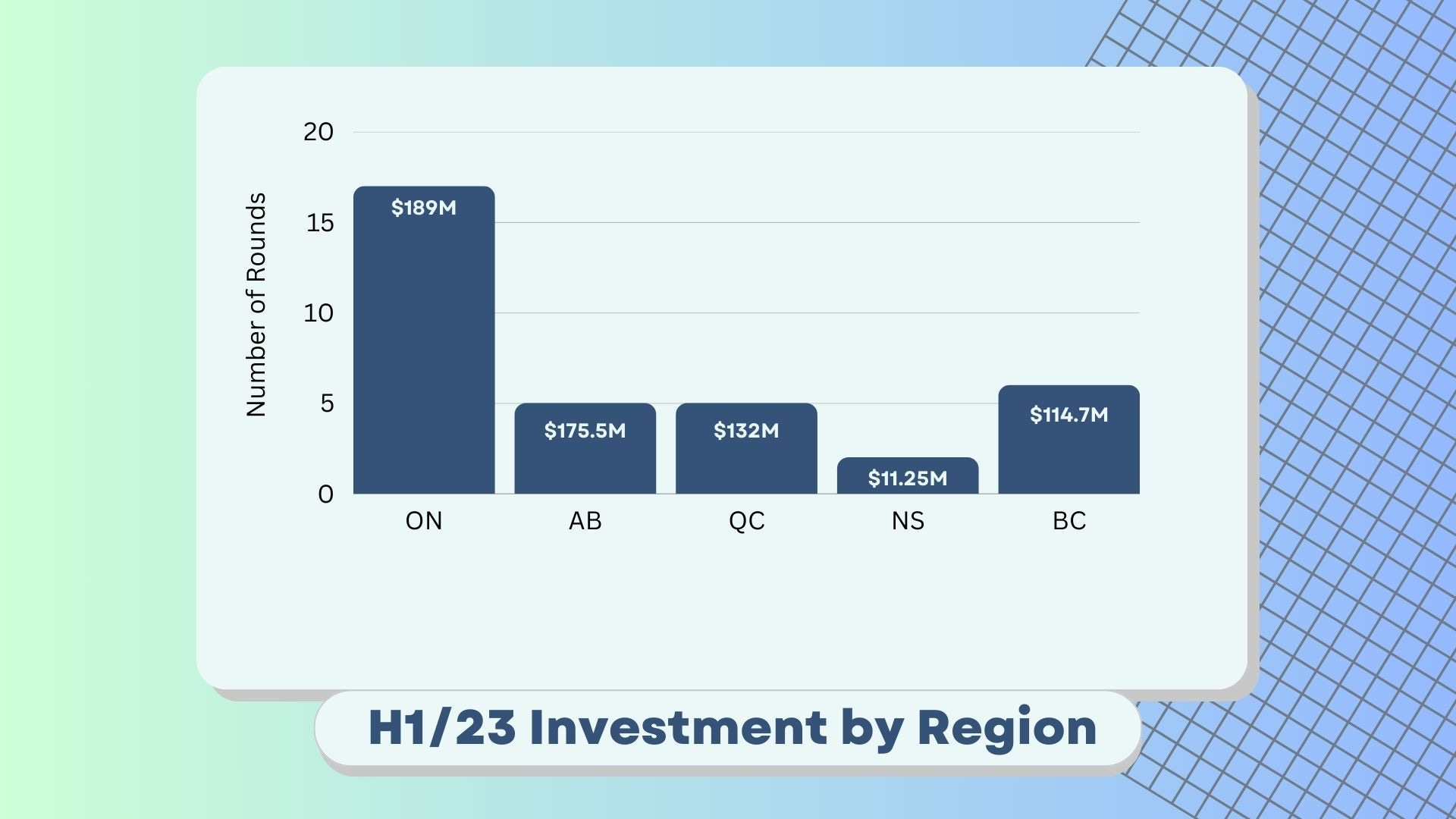

Ontario was the most active region in H1/23 with 17 rounds, and slightly more capital deployed than in Alberta and Quebec. Ontario-based companies bagged about 30% of all capital, while Alberta took home ~28%.

Ontario’s high activity is a consistent trend both from Q1 to Q2 and year-over-year, though total funding is more variable.

Funding sources

I wanted to dig into where venture capital is coming from. Are Canadian VCs backing home-grown companies? Are Canadian climate ventures securing international dollars? Who’s leading these rounds? Some high-level findings:

In H1 of this year, Canadian VCs participated in 61% of all rounds tracked and led the round 39% of the time.

Looking at all VCs participating in H1, 36% were based in Canada, 49% in the US and 11% in Europe.

Other than VCs, the most active investors in these rounds were strategic investments from industry or corporate venture (17 rounds), private equity/investment firms, and government-backed funds like BDC Capital (10 rounds).

Putting it in context

Canadian venture at large: I wanted to compare this data to the broader Canadian venture market, which saw a total $2.8B deployed across 170 deals in Q2.

For all Canadian venture in Q1 to Q2, total dollars raised increased by 140% and deal activity increased by just 3% according to CVCA. Year-over-year, total dollars raised dropped by 40% ($6.7B in H1/22 to $3.9B in H1/23) while deal activity dropped by 18%.

Global climate venture: According to CTVC’s numbers, venture & growth equity investments in climate dropped 40% YoY, from $21.8 in H1/22 to $13.1 billion in H1/23. Global deal activity grew by 8%, and deal size declined by 44%.

TL:DR; The YoY drop in funding is part of a wider trend we’re seeing in the Canadian market and in global climate. However, climate funding hasn’t seen the same uptick in Q2 like the rest of the Canadian market has. The bright spot is the increase in deal activity which is growing more than the global climate market.

That wraps up my take on the Canadian venture landscape for climate in H1. Do you have a diverging take on these trends or are seeing/hearing different things out in the market? Let me know by hitting reply, or find me on X or BlueSky.

Methodology

Capital: I reviewed every round to make sure it was either venture or growth capital and cross-referenced with other sources like Pitchbook. Private equity, government funding, project funding, loans, etc. were excluded as much as possible.

Climate tech: broadly, I consider climate tech to be companies creating technology that is intentionally reducing emissions, adapting to climate change, or helping monitor and quantify climate impact. I used Climate Tech VC’s classifications for Vertical and Industry.

Caveat: We’re dealing with a relatively small number of deals in this dataset that have a huge range of values. E.g. if I use a median to look at deal size (which is typically better for data with large outliers), we’re pretty similar to the global average. But using an average results in a 64% decline. So take these numbers with a grain of salt.